Private Lending – Perhaps not the “Oldest Profession”, but certainly the oldest form of lending.

Why are Investors, Finance Brokers and borrowers drawn to First Mortgage Private Lending?

Our comments in this Bulletin generally relate to peer-to-peer loans secured by a registered first mortgage over real estate. This is a personal business. It should be distinguished from second and third tier “institutional” funding, such as mortgage funds or the like.

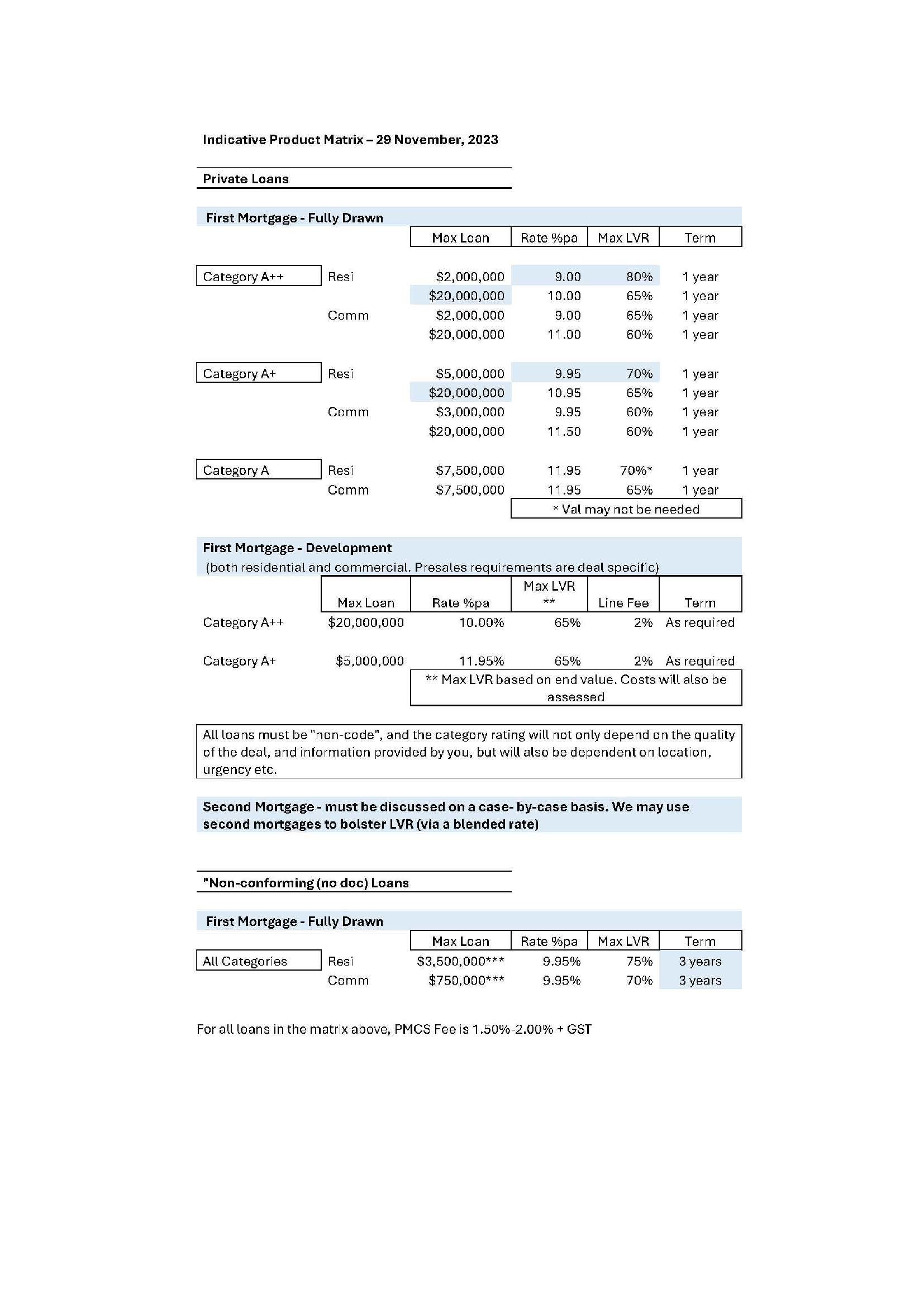

In the Indicative Product Matrix below, we have set out various criteria for your greater understanding. This Bulletin does not set out to be a comprehensive guide though, and there is no substitute for personal contact.

Genuine “home office” private investors may be more flexible in their investment strategies than are traditional banks or other lending market participants. There are few bureaucratic layers between investor and borrower.

Put simply,

1. In an environment of rising interest rates and high inflation, investors are looking for “real” income protection as a hedge against inflation. Interest rate returns from P2P first mortgage loans may be significantly higher than from other forms of fixed interest investment. Given the short-term nature of most loans in the private market, the interest rate reset factor is also attractive.

2. Borrowers seek greater reaction time, commercial flexibility and deal certainty to justify the price (interest rate) premium charged to borrowers by private investors. Flexibility works both ways, allowing the investor greater scope for capital preservation, obviously fundamental to their position. I look forward to hearing from you as a potential lender or borrower.

Steven Acworth

(Email) steven@sma.fund (Ph) +61 488 22 44 16